There was a guy in Russia who was their hyper-inflation coming beforehand. He took out as much fixed rate debt as he could to buy land, real-estate, businesses, etc. After the hyper-inflation he paid it all off for virtually nothing and became one of the richest men on the planet. This has worked for people in the past.Like it or not. The people in charge will monetize the debt. I want to side-step that elevator going down. By locking in a 30 year loan with 20% down. I will be paying off the balance with cheap printed up dollars when it costs a wheelbarrow full of cash to get a loaf of bread.

When post WW1 Germany started printing money, 1 US dollar was worth 4.2 marks. When Germany replaced that currency with a new currency based upon German Real Estate, the same 1 dollar would get you 4.2 Trillion Of the old marks

As much as I would like to be a Trilliionair, not If it means the dollar is on par with the Zimbabue currency. This is the path they are going down.

In any situation there are 3 types of people:

Those who know what is going to happen before it happens.

Those who know what is happening, while it is happening.

The rest are wondering? What happened?

those who refuse to learn from history are doomed to repeat it.

The idiots in charge are using history as a roadmap as to how to destroy our country.

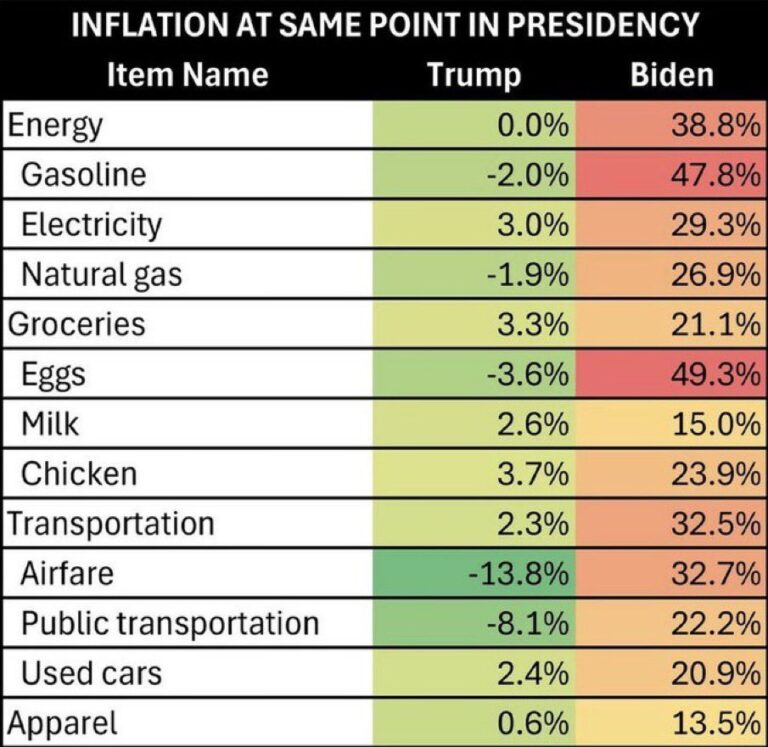

What is the definition of inflation? Too many dollars chasing too few goods.

Last year, where did they get the 1.9 trillion they handed out like candy? Did they tax it? Did they borrow it? Or did they print it ?

Printing money only devalues the dollar. I don’t want to own investments valued in dollars.

That being said, alienation clauses in mortgage contracts make it so that unless you have the capital required to immediately pay off your house at any time, then the lender could effectively, and legally, take your house and any equity you built up in it from you at any time on their whim. If the USD starts to hyperinflate then you'd better bet they're going to enact that clause rather than let you walk away with a home for pennies on the dollar.